Stablecoins: Bridge to Crypto economy

A primer on Stablecoins and increasingly important role they play

Stablecoins are blockchain-based digital currencies that are linked to the value of

an underlying asset. Blockchain technology enables a marketplace to operate without assigning control to any single participant. This can create good economic properties for fostering competition and innovation in the long run.

Owing to their peg, stablecoins are not subject to extreme price volatility, which has otherwise prevented mainstream adoption of applications built on top of

cryptocurrency protocols. The most commonly collateralized stablecoins are the ones linked to fiat currencies such as the USD, EUR, or GBP.

Stablecoins are free from the volatility of non-pegged cryptocurrencies, while inheriting some of their most powerful properties:

Stablecoins are open, global, and accessible to anyone on the internet, 24/7

They’re fast, cheap and secure to transmit

They’re digitally native to the Internet and programmable

How Stablecoins are formed

Approaches to developing a Stablecoin

There are three general types of stablecoins:

Asset-based stablecoins commonly use fiat currencies or precious metals as a peg to ensure stability. For example, Digix Gold Token (DGX) uses gold for its backing while Libra and Reserve were designed to rely on a basket of currencies.

Crypto-collateralized: Maker Dai (DAI) remains the largest cryptocurrency-collateralized stablecoin. The two cryptocurrencies backing DAI are ETH and MKR. Dai also uses smart contracts to ensure timely response to the main market tendencies in terms of changes in the demand and supply levels.

Algorithmic stablecoins rely on the rules written in the software code of the coin with the sole goal of matching the demand for the currency and its market supply. Kowala and Ampleforth are examples of non-collateralized or algorithmic stablecoins. Their mechanisms automatically adjust the levels of the supply, effectively ensuring stability.1

Quick history of Stablecoins

Total Stablecoin supply has reached $110B+ in July 2021, with USDT’s share at 60% (declining) and growing popularity of USDC now at ~25% share.

Stablecoin history begins with Tether, which runs USDT. Originally known as Realcoin, it began in October 2014. Tether’s model was always simple: It promised that for every USDT there would be an actual redeemable dollar in the bank somewhere. Tether faced various question marks and traffic bumps over the years - it shifted its collateral mix but still claims to be fully backed.

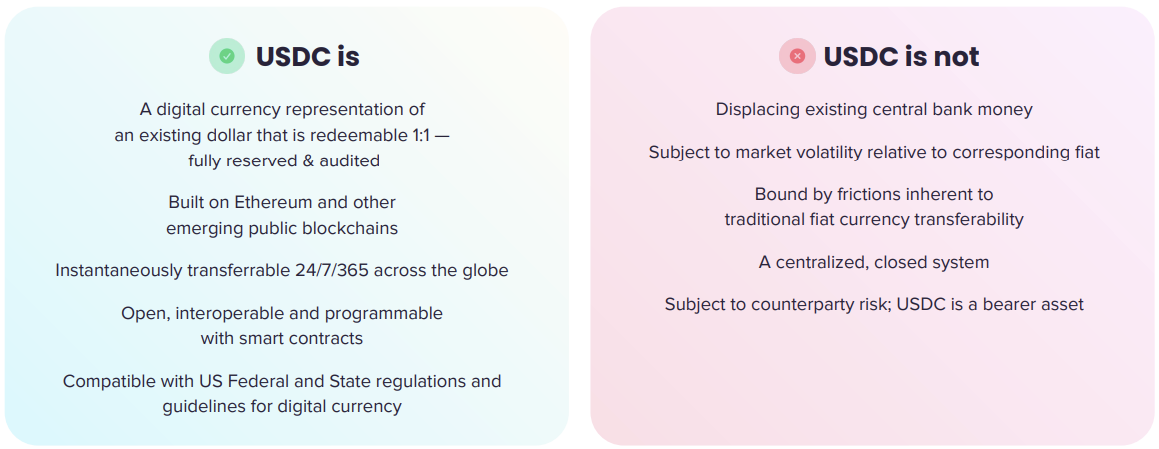

While this part of the market is established and it has worked well, those who want more regulatory confidence than USDT affords tend to turn to the CENTRE Consortium’s USD coin (USDC). The USDC stablecoin is fully backed and can be traded for the U.S. dollar on a one-to-one ratio through platforms like Coinbase and Circle. Like many other stablecoins, USDC currently operates on the Ethereum blockchain.

There are many others as well, such as Binance USD (BUSD) and TrueUSD (TUSD).

The next phase comes from over-collateralized but more decentralized stablecoins, such as MakerDAO’s DAI. DAI began as a stablecoin collateralized only with ETH, the cryptocurrency that runs the smart contract chain Ethereum. This required it to be seriously over-collateralized, at a minimum 150% but in practice usually much higher.

What are the main use cases of Stablecoin?

Without stablecoins, there would have been no decentralized finance (DeFi) booms, which means there probably would have also been no non-fungible token (NFT) boom. Stablecoins have been table stakes for what the industry has achieved so far.

Cryptocurrency Wallets/Trading: A digital wallet that stores private/public keys

and interacts with various blockchains, allowing users to send/receive digital

currency. Stablecoins could be used for crypto-trading on exchanges that cannot access banking services. It is also useful compared to legacy payments as they are instant and available 24x7. You don’t need a bank account to hold stablecoinsFiat Proxy in Decentralized Finance (DeFi): One can convert bank-based U.S. dollars into USDC and deposit it in a protocol like Aave to earn interest.

Global Currency: A stable digital currency can become a global medium of exchange (e.g., remittances), in markets with either hyper-inflation, economic

uncertainty, or capital controls.Cross-border Payments: Currently, global remittances can take days to settle and cost can be as high as double-digit percentages in some Emerging Markets. With stablecoins, remittances could be sent instantaneously around the globe at very low cost.

Trade Receivables Market: MakerDao, for instance is working with supply chain management startup Tradeshift, to tokenize unpaid invoices by selling them at a

discount to crypto investors, so that small businesses can receive their payment upfront.Offers individuals a cold store for USD/fiat by storing crypto in a medium that's disconnected from the internet and secured by one's own private keys.

Earn interest There are easy ways to earn interest (typically higher than what a bank would offer) on a stablecoin investment.

How These Projects Make Money

The key approaches of generating returns include their issuance and purchase. More often than not, stablecoins practice fractional reserve banking, meaning they do not represent 100% of the value as they claim. Other lucrative methods include:

the issuance and redemption fees

market-making activities, namely bid/ask spread and trading volume

a short-term lending

an annual reserve interest

However, other reasons can be branding and fund protection. Companies developing a stablecoin may want to create a safe virtual currency to pay their developers seamlessly. Furthermore, they aim to avoid losing money over time or attract users to other products in their portfolio, which is a vivid case of exchanges like Huobi, Binance etc. The investors purchasing stablecoins may use them to diversify their portfolio and preserve the capital during the bear market. The entities purchasing stablecoins may also generate return during the periods of small fluctuations.

How does it all work

Behind all of these new generation stablecoins, there’s one key insight which all of them rely on: the only thing that matters for a stablecoin is how well it can maintain $1 parity. Over the past year especially, we saw MakerDAO despite being 150%+ collateralised, failed to maintain an accurate peg.

Why would a coin which has tons of collateral backing it fail to maintain its peg? The short answer is the forces of supply and demand apply to everything including so called “$1” coins. So really, what all of these new stablecoins attempt to do is balance out the forces of supply and demand through their own unique ways. What’s fascinating to see is that the idea is rapidly evolving and each model iterates on the one prior to it.2

There are 4 stablecoins mechanisms today:

Reserves: This means that the stablecoin can be redeemed for the underlying reserve. The reserves then were gold but today it could be a lot of things like on-chain collaterals or off-chain collaterals. It could be like a MakerDAO where you have a lot of different kinds of currencies like $ETH, $YFI or $AAVE. Or it could be off-chain collaterals like gold, US dollars, Japanese yen, etc. Reserves are used to create mechanisms to determine stablecoins with low volatility.

Dual Token: This model has one token that is stable while the other token absorbs the volatility. When prices go up or down the secondary token absorbs the volatility. The secondary token could do a lot of other things but the main purpose is to absorb volatility so that it does not impact the stablecoin.

Algo stablecoins: Stablecoin is defined by math. You can change the math if you want (e.g., multi-sig governance) or if the governance votes for it (e.g., DAO)

Mixed: A mixed mechanism is a combination of two or a combination of all of the mechanisms; these mechanisms need not exist alone. You can hedge against volatility in a variety of ways.

Wait, how is stablecoin any different than money?

Stablecoins vs. e-money

Money can be broadly defined to have the following attributes: (1) a unit of account;

(2) medium of exchange; and (3) store of value. While cryptocurrencies have often

been compared to money, a major deterrent has been their extreme price volatility,

making them an unreliable unit of account over time.

Stablecoins are cryptos designed to minimize price volatility. They achieve this by

pegging their value to a stable fiat/other assets. Despite their similarities to fiat

currencies, below are a few points that distinguish them from e-money:

Privately issued, not linked in regulatory framework: Stablecoins are

privately issued. For instance, the most popular stablecoin, USDT, is issued by

Tether International Ltd, a privately-held company. They are also not

automatically linked in the regulatory framework with central bank money.Underlying technology: Classic e-money tends to be limited to the purpose and

infrastructure of the issuing institution/business, while operating in a closed loop

system. In contrast, issuance of stablecoins on a decentralized network allows

for transfer of funds between businesses and people.Cost of liquidation into fiat: Costs for liquidation of stablecoins into fiat

currency can be higher versus e-money which tends to be near costless.

Stablecoins vs. Decentralized Cryptos

Decentralization, in essence, means no single central party has the authority or

power to control the operation or outcome of the process. A decentralized network

relies on host of computers to complete the process. Hence, blockchain technology

needs a P2P network. On the contrary, stablecoins tend to be backed by a single

base, and work more in a centralized pattern.

Decentralized cryptos do not have a central repository which could wipe out all the

holdings in case of a server crash or if the user misplaces his private key. This is not

the case with collateralized stablecoins which have equal or more asset base to rely

on. An interesting point here is that while private keys get lost all the time and the

pool of coins diminishes, coins could get over-collateralized with time.

Another difference would be the reason stablecoins were invented i.e., price

volatility. It is possible for decentralized cryptos to have large price variations as

opposed to stablecoins which are not very price sensitive (at least in theory). Some

coins are also pegged to the U.S. dollar, which links them to the U.S.

banking/financial system, and thereby rely on a centralized infrastructure.

Depending on the protocol, stablecoins can possibly transact faster than classic

cryptocurrencies. The Libra protocol technical document highlights “the system is

likely able to meet the demand of 1,000 transactions per second (TPS)”. By

contrast, Bitcoin has a transaction capacity of 7 TPS. Visa handles around 1,700 TPS (or 150 million a day) and claims to be able to handle up to 24,000 TPS, in theory.

Stablecoins vs. CBDCs

CBDCs, or central bank digital currencies, aren’t stablecoins. They’re just fiat in digital form, and fiat isn’t stable. The difference between a stablecoin and a CBDC is that one is a synthetic derivative of a fiat currency created by a private company, and the other (CBDCs) is strictly a fiat currency produced by a central bank. CBDCs, in relation to other CBDCs and cryptocurrencies, aren’t stable at all. Their only purpose is to allow transactions and show transactions transparently to make taxation easier for governments.

So, are there any risks with stablecoins?

What are the risks of putting cash into stablecoins? The risk is that the stablecoin collapses. Tether, as others have mentioned, has a somewhat sketchy history, while USDC is well documented to be much more organizationally stable. Maker/DAI functions using a complicated set of economic incentives and smart contracts, and there is a potential that either the economic incentives don't hold up, or that there is a bug in the smart contract. However, even in USDC, which uses a very simple smart contract, there's still the risk of a critical flaw being discovered.

Future of Stablecoins

It may be easy to forget, but the original idea of bitcoin was to create a decentralized and distributed payment system; that has not yet happened. What has happened instead, and a testament to the free market process, is that an alternative (some would say better) version of crypto has emerged in the form of stablecoins. To function effectively as a currency alternative, crypto must be liquid, possess relatively low price volatility, and be integrated with established financial institutions.3

Stablecoins have gained quite a lot of traction, mainly due to their price stability linked with collateral reserves. Stablecoins are used as base currency for trading and are commonly used on DeFi platforms which earn high interests for stablecoins lent/borrowed on the market.

Tether is already deemed ‘too big to fail’ - disclosures in May 2021 suggest Tether has become one of the world’s largest investors in the US commercial paper market, rubbing shoulders with the likes of fund managers Vanguard and BlackRock and dwarfing the investments of tech giants like Google and Apple. Its reserves include $30bn in commercial paper; such holdings of companies’ short-term debt would make it the seventh largest in the world.

Visa crypto cards have already racked up $1B in spending in 2021. The company’s crypto card program is part of a larger push that Visa is making to merge the crypto world with traditional banks that includes adding stablecoins to Visa’s payments network and plugging banks into cryptocurrency buy and sell features.

The global financial economy requires a payment system where you can make payments without any delay, and that is cost-effective and free from intermediaries; stablecoins can fulfil this need. With new stablecoins constantly being launched, soon there may soon be one that’s pegged by every fiat currency in the world or a basket of currencies.

As the governments are inclining more towards central bank digital currency (CBDCs), you may see state-issued collateralised stablecoins in the future. But the government may have all rights reserved for such coins. If you prefer decentralised tokens, you can opt for crypto-backed stablecoin.4

Follow me on LinkedIn

Nakul

If you liked this post from Cryptechie, please subscribe and share!